Banking Must Change

BRN Senate Submission Lays It All Out

It's time to change the way banks operate. It's all here: a people's bank; how to manage the risk of bank failure and even better how to prevent them. The Senate inquiry into regional bank closures was a great opportunity to spread the word about critical reforms. Banking must change to a system that supports the interests of the people and country. This is an emergency and if we don't act now we face a very bleak future. We will own nothing and be very unhappy .... just the way our rulers want. These reforms help turn the tables ..... a first step to the rulers owning nothing and being miserable.

Senate Standing Committees on Rural and Regional Affairs and Transport 22.03.23

PO Box 6100

Parliament House

Canberra ACT 2600

Phone: +61 2 6277 3511

By email only - rrat.sen@aph.gov.au

re: Bank closures in regional Australia

BRN welcomes the opportunity to contribute to this inquiry.

Terms of Reference.

a. the branch closure process, including the reasons given for closures;

b. the economic and welfare impacts of bank closures on customers and regional

communities;

c. the effect of bank closures or the removal of face-to-face cash services on access

to cash;

d. the effectiveness of government banking statistics capturing and reporting regional

service levels, including the Australian Prudential Regulation Authority's

authorised deposit-taking institutions points of presence data;

e. consideration of solutions; and any other related matters

Upper echelon bank executives are amongst the highest paid and most powerful people in the world.

If a problem arises or an issue needs urgent progressing the CEO clicks fingers and the issues are sorted by skilled problem solvers. A "whatever-it-takes" attitude makes sure that the bank's interests or goals are not threatened or derailed. Thus the major banks have the ability and capacity to halt and even reverse .... operation branch closure .... if they so choose.

Customers - particularly in regional areas - on the other hand, appear to be a second or third order priority. They can have their lives and businesses disrupted in a very significant way simply to suit the interests of the bank. No other business can even try and get away with this sort of approach to customers.

It appears that the Big Four banks have little insight into the ramifications to their businesses if they continue along the path they now tread.

Banks want to close branches and bring about the end of cash for several reasons. A big one is to lock people into a system where banks get a cut of every single transaction made in the country. Transaction fees will of course rise when people don’t have the cash alternative.

A major element of maintaining savings bank services in regional areas is to put in place a competing banking service that serves the people’s interests. The private banks can then continue to close as many branches as they like while people choose to bank where they like – at the people’s bank set up through the licensed Post Office network.

The time has come - a National Australia Post Saving Bank network is now a critical reform. Banks working in people’s interests may seem novel but there are important precedents – look up the Bank of North Dakota and related information.

Hard to get ahead

Why is it so hard for people to get ahead and improve their lives right now? Why has the progress that capitalism promised not been delivered? Simple – the country and its people are being robbed! The colourful movers & shakers have followed the money and are stealing it from right under our noses. Regulatory bodies such as ASIC have let the people down by failing their purported role. If it wasn’t for the corrupted financial system and its interaction with poor government policy the cost of living would be around 30 to 50% lower than it is now.

The finance sector has been allowed and enabled by governments to siphon away far too much of the nation’s wealth. Individuals working in the financial sector have experienced a disproportionately huge increase in their incomes relative to workers in other sectors while too many Australians are becoming poorer. This can be clearly seen by the cost-of-living pressures people are now facing – particularly regarding the housing affordability crisis. This is a predictable result of the “financialisation” of the economy. This was exacerbated by the terrible government and bank policies preceding, during & following the 2008 GFC and then again with the inflationary money printing and mega-low interest rate environment during the COVID response.

The current system has created a perverse incentive whereby bank CEOs and executives chase short-term financial returns in ways which can and do cause long term damage to a bank’s core business and its customers’ financial wellbeing.

What is the government’s preferred solution to improve “productivity” and GDP? Increasing the population by 400,000 people per year! This will continue the housing bubble (the main aim of the policy) and the related rental crisis while boosting GDP BUT reducing per capita GDP – i.e. they aim to continue the squeeze on families who will also have to deal with worsening access to important services and infrastructure.

Government policies have greatly contributed to the creation of a pathological society - one that does not suit human beings. It is in large part responsible for problems such as: drug & alcohol abuse, domestic violence, divorce, mental illnesses such as anxiety & depression, suicide, even much petty criminal activity is a response to the difficulty many people have getting a fair go. The petty crooks swell our jails. The big crooks rule the world and drive nations into unsustainable debt – never to be repaid but forever subjecting citizens to the use of debt and taxes as tools of subjugation and weapons of mass exploitation.

For banks, political donations are a very good investment if they stop governments from interfering in the banks’ business model and goals. Watch this issue carefully as it could be one of the biggest market manipulations in Australian corporate history. Just imagine if the Big Four banks are colluding to force the abolition of cash via branch closures, removal of ATMs, and directing staff to force customers into the digital net.

Another reason people find it hard to get ahead is a similar confiscation and diversion of their wealth into the hands of the military industrial complex. Without this theft benefiting the finance sector and the war machine taxes could be much reduced.

Reform is now urgent

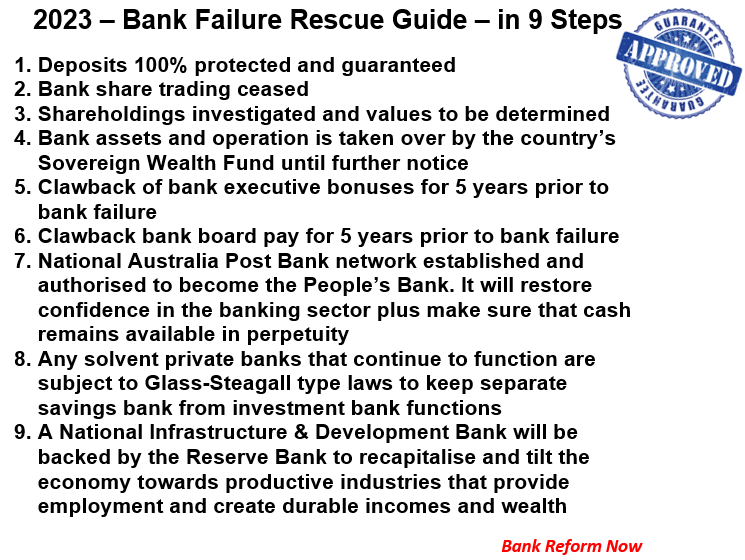

The number one reform requires us to realise that basic banking is really a critical utility. BRN refers to the reform required as a Sovereign Monetary System. A savings bank is a relatively simple operation that is not really that profitable. Governments have allowed the banks to profit from credit creation as well as complex and opaque investment banking which should be totally separated from the banks’ core business that is provided to the vast majority of savings and loans customers. Banks are really using their customers’ funds to generate income for their shareholders and upper-level executives. In other words, the aim of the game is not to serve their customers – it is to exploit them. When the bankers’ gambles and manipulations turn sour, they expect to be bailed out by governments, taxpayers and customers. The classic moral hazard scenario – see below regarding nine critical steps to protect depositors and the country when a bank failure threatens.

There are two main ways to sort this out. One is totally unacceptable …… nationalising all the banks. Therefore, our politicians must support and facilitate the alternative …… a National Australia Post Savings Bank. The private banks would have to compete. Their operations would gradually change. The risky speculative banking services would be available for those who want them. Most people will want a people’s banks. The profits of credit creation are much like a country’s natural resources. In our opinion they must be returned to the people via a Sovereign Wealth Fund.

Reform is required but it must be done thoughtfully and carefully to moderate the significant reduction in property and share values that are likely in 2023 - 2024. We suggest that when house values go down the banks should bear a good portion of the losses as part of the reform process – not the people who have been exploited, often by predatory business practices. Sorry to say, but property prices really should come down by at least 50% as part of the repair work. Trying to boost wages or build more cheap housing will not do the job required. Australians on normal incomes should be able to afford proper housing! Has Australia got the leadership capable of delivering this?

Irresponsible and excessive bank lending - as well as greed & stupidity - have fuelled the unsustainable property market. The Banking Act still contains the provision that allows the RBA to order the banks to reduce the lending that has led to an imbalance – ie a bubble. For some unknown reason the RBA just hasn't used these (Ben Chifley) laws effectively - they seem to have missed the boat. In a "correction" the RBA could support the banks to write down their balances on their mortgage loans, to match the new values.

Additional comments and related matters

The current turmoil in banking that we are seeing in Europe and America are just signs and symptoms of a flawed unsustainable system once again becoming unstable. We have seen decades of bank scandals involving: predatory lending; fraud, forgery; asset stripping of farmers, retirees, small businesses & “unsophisticated” investors; rate rigging; commodity market manipulation; money laundering; drugs & arms trafficking; terrorism funding; financial planner scandals; managed investment scheme scandals; insurance scandals; and tax evasion.

Corporations are often aided in corrupt behaviour by their links to political parties. Political donations are an associated area that requires reform. Firstly, we need to be clear that no business or corporation gives money to a political party without expecting the gesture to be helpful in some way to their business. BRN has proposed that no individual can donate more than $1,000 per year to the party of their choice – and they should only be able to donate to one party.

Businesses (and unions) should not be able to donate at all. Fundraisers such as $20,000 per plate dinners where a businessman can sit at a minister’s or shadow minister’s table are not acceptable. The beauty of our proposed system is that the only way for parties to raise donations is by earning trust and respect from ordinary voters. This is done by displaying integrity, honesty, and wise policy formulation - good for our democracy and good for our people.

Also good for our democracy would be reform of political advertising – political parties should not be permitted to use advertising companies at all. We don’t want the party with the best ads on TV to govern us. We need the party with the best people and policies. “Advertising” should only consist of ministers discussing policies and facts – simple and clear. If a politician (and party) cannot do this without a slick marketer holding his or her hand they clearly are unsuited to the job.

Every candidate that runs for election should have a web page hosted on the AEC website. On that page there can be a video explaining their policies and some related information. The AEC runs ads in print, radio, TV, and web portals giving the link to the site where the information can be found. Voters can visit the site to find out what their candidates stand for and offer.

Another benefit of these policies is that political parties will not need the volume of donations that are now undermining our politics and democracy.

Key Points:

A) Banks are closing branches as part of a worldwide push to force populations into a cashless society. This has been well documented over many years in International Monetary Fund (IMF) and Bank for International Settlements (BIS) publications. For example – BIS head Agustin Carstens about CBDC and control >> https://www.youtube.com/watch?v=rpNnTuK5JJU

B) While many citizens do enjoy the convenience of digital banking via cards and phones, they often do not understand the downsides. The government should educate the population on the importance of maintaining cash as a key part of the economy and an important protector of their privacy and freedom. (See below for BRN Fact Sheet – The War On Cash Must Be Won).

C) The banks are hastening the decline in the use of cash by removing face to face banking and access to ATM machines.

D) Bankers and bank boards must be held accountable for the business practices they engage in and encourage that threaten their depositors’ funds and the stability of the banking system. Clawbacks and other methods will deter malfeasance and other dangerous business activities. This will also assist in countering the moral hazard issue.

E) Bank deposits should no longer be considered an unsecured loan by a customer to the bank. This changes the whole business model of banking. This change is long overdue.

F) Reforms must be introduced regarding political donations and advertising.

___________________________________________________________

2023 – Bank Failure Rescue Guide – in 9 Steps

___________________________________________________________

Thank you for your interest and time on this important issue.

____________________________

Dr Peter Brandson

CEO Bank Reform Now

www.bankreformnow.com.au

www.facebook.com/bankreformnow

| Attachment | Size |

|---|---|

| 319.77 KB |

Share This Page

Print PDF

Print PDFRecent News & Articles

Latest News & Articles

Bank Victims Horror Stories

From Extend RC Parliament Event

>> See ALL Horror Stories List